Is AMD Undervalued After The Latest GPU Release?

Comparing Nvidia vs AMD latest release of GPU. The ability for AMD to potentially carve out a sizeable portion of the AI data center market share.

Nvidia vs AMD: How the Latest GPU Releases Will Set the Stage for AI’s Next Decade

AMD aims to compete NOT by beating Nvidia everywhere, but by being GOOD ENOUGH where it matters most

Introduction: The GPU War That Will Define AI in 2026+

For the past several years, Nvidia has been synonymous with AI. If you trained a large language model, ran a hyperscale data center, or built an autonomous system, chances are it ran on Nvidia GPUs.

But 2026 marks a structural shift.

With Nvidia’s Rubin R200 and AMD’s Instinct MI400 series, we’re no longer just talking about faster chips. We’re talking about who controls the economics of AI compute as the industry moves from experimental training runs to always-on, real-world inference at planetary scale.

This article breaks down:

- Why AI compute demand is exploding toward Yottascale

- How Nvidia Rubin R200 compares to AMD Instinct MI400 in practical terms

- Why Nvidia has been nearly impossible to dethrone (CUDA vs ROCm)

- Why ROI, cost, and workload segmentation may finally open the door for AMD

And most importantly:

Why 2026 could be the year AMD stops being “the alternative” and starts being essential.

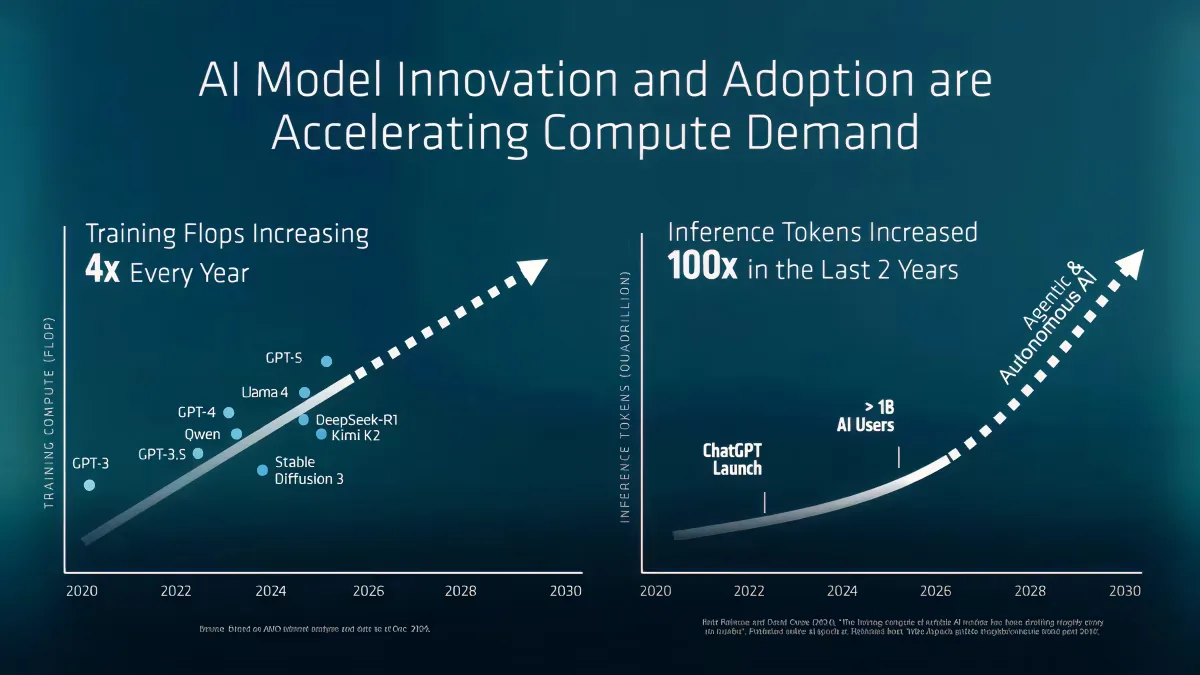

1. AI Compute Enters the Yottascale Era

From Zetta to Yotta: A 100× Shock to the System

When ChatGPT launched in 2022, global AI compute capacity was estimated at roughly 1 zettaflop.

Fast forward just a few years:

- Global AI compute capacity has surged nearly 100×

- We are approaching 100 zettaflops

- And we are now racing toward Yottascale

This is not linear growth. This is an infrastructure shock.

How Big Is Yottascale, Really?

To make this concrete:

- 1 Exaflop = 1018 Operations Per second

- 1 Zettaflop = 1,000 Exaflops = 1021 Operations per second

- 1 Yottaflop = 1,000,000 Exaflops = 1024 Operations per second

Why This Leap Is Happening: The Shift to Inference

Training large models made headlines.

Inference is what breaks the grid.

We’ve crossed a critical inflection point where AI demand is no longer driven by training alone, but by Inference at Scale:

- Autonomous agents running 24/7

- Multimodal systems processing text, images, video, 3D, and sensors

- Continuous reasoning, not single-prompt responses

- Embedded AI inside enterprise workflows, robotics, logistics, and finance

In simple terms:

AI is no longer something you ask.

It’s something that’s always working.

From Assistive to Transformational

Reaching Yottascale unlocks capabilities that were previously impossible:

- Healthcare: Real-time diagnostics, protein folding, and drug discovery

- Climate science: Ultra-high-resolution weather and physics simulations

- Physical AI: Autonomous factories, warehouses, and transport networks

- Hyper-personal agents: Always-on copilots managing your work and digital life

Zettascale got us smart assistants.

Yottascale gives us autonomous systems.

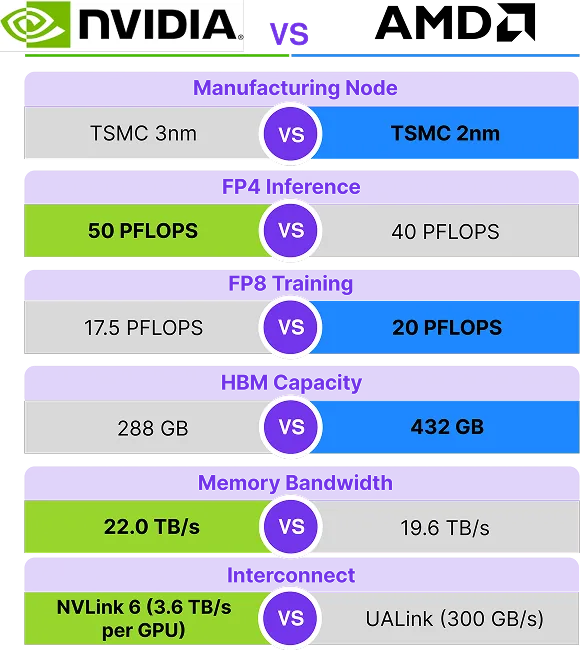

2. Nvidia Rubin R200 vs AMD Instinct MI400: What the Specs Actually Mean

Before diving into numbers, let’s translate GPU jargon into real-world impact.

What These Specs Mean (In Plain English)

- Manufacturing Node: Smaller nodes = more transistors = more performance per watt

- FP4 Inference: How efficiently the GPU runs everyday AI queries

- FP8 Training: How fast models can be trained or fine-tuned

- HBM Capacity: How much “working memory” the GPU has for large models

- Memory Bandwidth: How fast data moves between memory and compute

- Interconnect: How well GPUs talk to each other at rack scale

AI is rarely limited by raw compute alone.

Side-by-Side Comparison

Manufacturing Node: Nvidia - TSMC 3nm vs AMD - TSMC 2nm

FP4 Inference: Nvidia - 50 PFLOPS vs AMD - 40 PFLOPS

FP8 Training: Nvidia - 17.5 PFLOPS vs AMD 20 PFLOPS

HBM Capacity: Nvidia - 288GB vs AMD - 432 GB

Memory Bandwidth: Nvidia - 22.0 TB/s vs AMD - 19.6 TB/s

Interconnect: Nvidia - NVLink 6 (3.6 TB/s per GPU) vs AMD - UALink (300GB/s)

The Key Takeaway

- Nvidia still wins peak performance and scaling maturity

- AMD is optimizing for cost-efficient inference at scale

This difference is not accidental.

It reflects where each company believes the market is going.

3. Why Nvidia Has Been Nearly Impossible to Dethrone

Nvidia's CUDA vs AMD's ROCm: The Real Moat

Nvidia’s dominance isn’t just about silicon.

It’s about CUDA(Compute Unified Device Architecture).

CUDA is not a programming language.

It’s an entire AI civilization built over 15+ years.

Foundational models, research pipelines, tooling, debuggers, libraries, and frameworks have all been optimized for Nvidia hardware.

Switching GPUs isn’t as simple as unracking old GPU and replacing with a new one.

It requires:

- Rebuilding software architecture

- Refactoring CUDA-optimized kernels

- Re-validating performance and accuracy

- Re-training engineering teams

- Accepting uncertainty in performance parity

Even if ROCm (Radeon Open Compute Platform) is technically capable, migration cost is massive.

This is why Nvidia could command premium pricing:

Customers weren’t just buying GPUs — they were buying for the whole build.

Why This Is Finally Changing

Three things are breaking this inertia:

-

Inference Workloads Are Less Sticky

Many inference tasks don’t require custom CUDA kernels. -

Cost Pressure Is Back

ROI is replacing “buy whatever Nvidia ships.” -

Hyperscalers Can Force Change

When OpenAI, sovereign funds, or hyperscalers commit, ecosystems follow.

This is where AMD enters the conversation — not by beating Nvidia everywhere, but by being good enough where it matters most.

4. The Market’s True Desire: ROI Over Brute Force

AI Will Segment by Complexity

The future AI stack will not be uniform. It will stratify.

A) High-Complexity Workloads (Nvidia-Dominant)

- Scientific simulations

- Advanced mathematical modeling

- Autonomous agentic systems

- Financial modeling and real-time trading

- Robotics and physical AI

These workloads demand:

- Peak performance

- Mature tooling

- Guaranteed scaling behavior

Nvidia remains king here.

B) Mid-to-Low Complexity Workloads (AMD’s Opportunity)

- Document summarization

- Search and retrieval

- Customer support AI

- Enterprise copilots

- Routine inference tasks

These workloads represent:

The majority of AI consumption.

They don’t need maximum performance.

They need cost-efficient, reliable throughput.

This is where AMD shines.

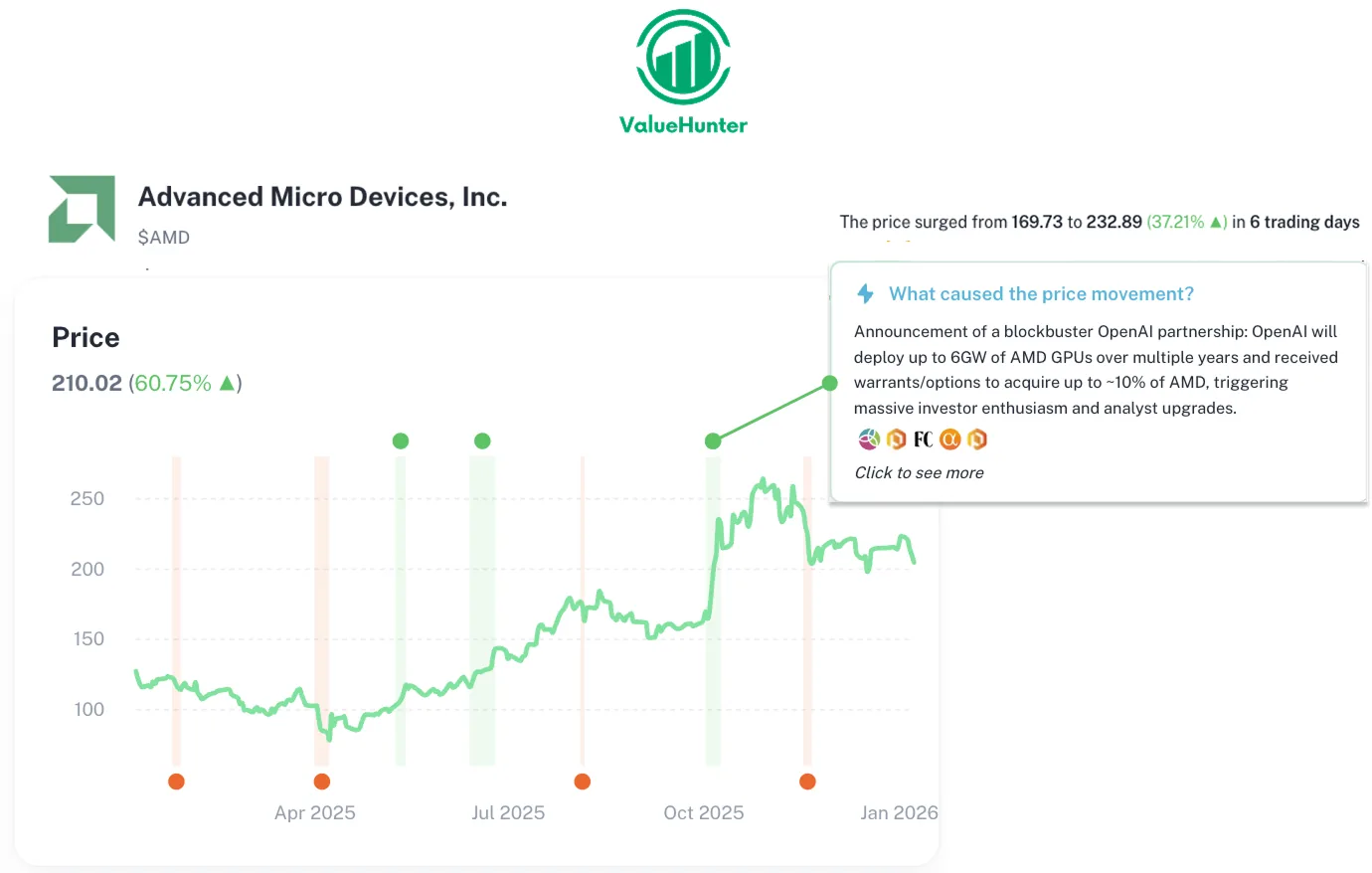

The Catalyst: AMD, OpenAI, and the 6–10 Gigawatt Bet

The OpenAI Deal That Changed Everything

- 6 gigawatts of AMD Instinct GPUs (MI450 / MI500 series)

- Built toward OpenAI’s Stargate project

- Total capacity potential: 10GW

- Implies AMD supplying ~60% of a major AI player’s compute

Even more striking:

- OpenAI is reportedly allowed to take up to ~10% equity stake in AMD

This isn’t a vendor relationship.

This is strategic partnership.

Now everything hinges on one thing:

How does the shift over to MI455X fare for OpenAI compared to what it has always been with Nvidia?

If it’s “close enough” and “easy enough,” the market changes overnight.

Cracks in the Monopoly

We’re already seeing it:

- Saudi sovereign AI deals split between Nvidia and AMD

- AMD winning smaller but strategic footholds

Deals AMD wouldn’t have even been invited to five years ago

Nvidia still wins the bigger checks.

But AMD is finally in the room.

Market Share Reality Check

- Nvidia: 90–95% of AI data center GPUs

- AMD: ~4% today

But measured in gigawatts of deployed compute, AMD is moving into double-digit share.

That’s not symbolic.

That’s structural.

The Valuation Question No One Wants to Ask (But Should)

Nvidia market cap: ~$4.6 trillion

Market share: ~90–95%

If AMD captures:

- 10% AI compute share → $460B implied value

- That’s roughly 35% upside from current levels

- Now imagine if AMD takes 15% or 20% of the market share

And remember:

Most AI workloads are not high-complexity.

As AI architectures mature, ROI-driven compute allocation becomes inevitable.

That future favors AMD.

Conclusion: 2026 Is AMD’s Moment

Nvidia will remain the performance leader.

That’s not in dispute.

But the AI market is no longer about who is fastest.

It’s about who is economically scalable.

AMD doesn’t need to dethrone Nvidia.

It needs to become indispensable.

With:

- Lower cost solution for majority consumer AI usage

- Strategic OpenAI alignment

- Growing sovereign and hyperscale wins

- A market shifting from brute force to ROI

AMD is no longer just the underdog.

It’s the pressure valve for an AI industry racing toward Yottascale.

Next Steps

Disclaimer: The information provided is for educational purposes only and should not be considered financial or investment advice. Always do your own research

For latest news and deeper dive into AMD (click here)

For latest news and depper dive into NVDA (click here)

Log in to start your own research and stay informed

Sources:

https://www.amd.com/en/corporate/events/ces.html

https://www.amd.com/en/newsroom/press-releases/2026-1-5-amd-and-its-partners-share-their-vision-for-ai-ev.html

https://www.amd.com/en/blogs/2026/from-ces-2026-to-yottaflops-why-the-amd-keynote.html

https://www.amd.com/en/newsroom/press-releases/2026-1-5-amd-expands-ai-leadership-across-client-graphics-.html

https://blogs.nvidia.com/blog/2026-ces-special-presentation/

https://nvidianews.nvidia.com/news/rubin-platform-ai-supercomputer

https://www.nvidia.com/en-us/events/ces/